{Forest Patchwork Wallet by Faith on Earth}

It occurred to me a while ago that I was not doing anything to plan for my retirement.

Of course, I never really plan on ‘retiring’ per se – I think I’ll be one of those people who’s doing some sort of work till the day I die – simply because otherwise, I’d get terribly bored.

However, it seems only common sense to ensure I have enough money for my old age should something prevent me from being an internet-savvy old woman, right?

If you’re a passionate, self-employed entrepreneur, I’ll bet you probably have the same dreams for your old age. But do you have a retirement plan in place in case you can’t work forever?

Now, Nick and I do own a house in England, so that’s one part of our retirement plan, but that in and of itself won’t be enough to see us through. We need to start putting money away for the future, and as the breadwinner, it’s my responsibility to make sure this is happening.

I’m not an anti-money-creative-type. I actually thrive on the money side of my business. I love knowing how much I’m earning week-to-week, knowing how much I’m spending.

I love setting money goals.

We keep on top of all the business income and expenditures so we always know where we’re at – and if you don’t, I HIGHLY recommend you start. Because if you don’t know what’s going on in the financial side of your business, it’s my opinion that you don’t have a business, you have a hobby.

So, the fact I’ve let this slide for the last few years is surprising, and something I’m relieved to have taken the time to think about.

Like the rest of my fellow Aussies, I have a Superannuation account (or Super, as we call it). For those of you outside of Australia, Super is a government-mandated retirement fund that every working Australian must have, and their employers are legally bound to contribute money into this account on their behalf.

So, I have some money in a Super fund from when I had a ‘regular’ job – but I haven’t remembered to put any additional funds in there for the last few years that I’ve been self-employed.

BIG money fail on my part.

However, unless you want to go to the trouble of putting together a self-managed Super fund, you don’t have a whole lot of control over where your money goes – my Super fund is managed by a company who invest the money on my behalf. And considering how many people near retirement age lost a huge chunk of their Super with the last GFC, I’m actually not all that keen on putting all my retirement eggs in the share market basket.

So, I’ve done the simplest, easiest thing to start off with – set up an automatic savings plan.

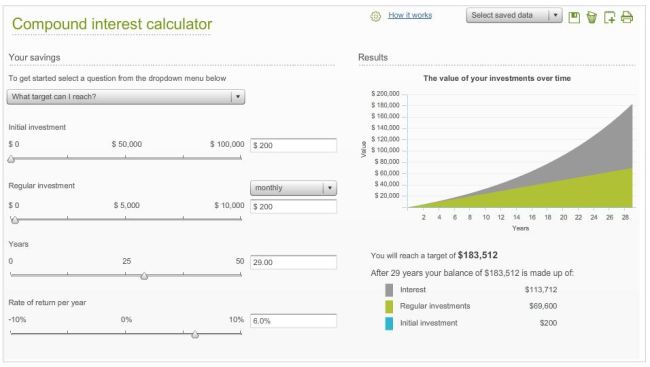

At the moment, $200 a month goes straight from my regular account into a dedicated retirement savings account that receives a good interest rate.

Simple.

The key here? You need to make sure it’s HARD to get the money out of your retirement account. You need to basically forget that money exists.

There are a few great online bank accounts you can get here in Australia that meet these conditions – like an ING or UBank account (I have accounts with both for different reasons). If you have one of these accounts, you can make sure your retirement money is completely separate from your regular money, and you don’t have a keycard that lets you access it.

We’re also lucky here in Oz to not have completely horrendous interest rates at the moment (horrendously low, I mean) – you can get an account with that will give you around 5% p.a. return (at least at first…).

That might not sound like much, but check this out:

If I just put that $200 a month away in a regular account, I’d have just $69,600 by the time I hit 60. With a 6% interest rate (I’m assuming it will be more and less than this over the years, but it’s a nice believable average) I end up with $183,512.

Pretty amazing. And all for just putting aside $200 a month over 29 years, and never touching the capital.

If you want to play around with this calculator yourself, you can find it here.

Another important piece of the puzzle is my Super – I can’t totally neglect that.

However, I don’t want to put lots of money in there because 1) I only have a very basic level of control over where that money is invested 2) I can’t access that money until retirement age.

As much as I never, ever want to touch my retirement account, I still have the security in knowing it’s there should something catastrophic befall me and Nick, and we desperately need the money – for a life-saving operation, or some such.

But, I’d be missing out if I didn’t take advantage of the Australian Government’s Co-Contribution Scheme.

“The superannuation (super) co-contribution is a government initiative to help eligible individuals boost their super savings for the future.

If you are a low or middle-income earner, you can take advantage of the super co-contribution payment by making eligible personal super contributions to your super fund or retirement savings account (RSA). The government will then match up to $1,000 of your personal super contributions.

You don’t need to apply. If you’re eligible, all you need to do is make eligible personal super contributions to your super fund or RSA and lodge an income tax return.”

So, let’s add to my plan – putting $1000 per year into my Super, to get what is basically a free additional $1000 from the government each year towards my retirement. I’m kicking myself that I’ve let that slip through the cracks for a few years now.

After writing this all down and getting it straight in my head, I’m feeling a lot better about my long-term financial future.

So, in short, my plan is:

1. Set up a $200 auto-payment per month that goes into a ‘forget-about-it’ retirement account.

2. Put $1000 into my Super account at the end of each financial year to take advantage of the Australian Government’s Co-Contribution Scheme (This site/resource is no longer available.)

.

3. Care for our current investments to ensure they’re giving us the best return possible (house rent and shares).

So, that’s my take on a simple retirement plan for the self-employed.

At least, it’s a start!